Hi,

I am helping an elderly family friend with his home in London. A decorator/builder pointed out cracks and uneven door frames and said this was subsidence. I contacted a friend who has experience renovating houses who (logically I think) advised me to call the insurance company, since we are lay people in this regard and have them take a look to see if it is or it isn't. I did so, but just getting them to evaluate it involved "making a claim" which made me apprehensive.

OK I've descended into a story, so instead I will just summarise what people have told me, which will hopefully be clearer (though you will see why I am very confused). I have included photos of the cracks at the end.

Friend with experience renovating houses: subsidence he associates with cracks from the base of the property, of which there are none (at least not visible) in this case. He says cracks/movements around doors and bay windows are quite common as these are weak points susceptible to settlement.

Neighbour who has been on the road for a long time and pretty much knows about everything that is happening here: he laughed at me saying these are not cracks! He says they have been there for a very long time (this corresponds to what the family friend/owner of the house says) and they are just the result of settlement. He knows only of one house on the street that had subsidence and this was because of a bad tree the council planted (they are – ahem I mean we are – footing the bill) and says he can’t recall there ever being a large tree outside the family friend’s house. He says he has worse cracks that he is not concerned about at all. He warned about getting a ‘history of subsidence’ on a property (this corresponds with what I have read).

Insurance lady: so at this point I call the insurance lady saying how foolish I am and that this is probably nothing. Interestingly she echoed what the friend with experience renovating houses said about no cracks at the base of the property, saying that based on the description I gave this didn’t sound like subsidence to her. She says not to worry, that the insurance claim can be withdrawn and because the value on it would be zero, this should not affect premiums. However, she asks me to get a builder to look at it just to be sure. In hindsight this seems a bit strange since I don’t think the average builder would be qualified to say, or at least would be unwilling to make an assertion, unless perhaps it was very clear-cut, e.g. superficial cracks in the plaster.

Friend (former estate agent) and her friend, an expert in building materials: This is where it gets confusing. So, I contact the friend to ask if she knows a builder that would be suitable. Her friend, in Poland, is an expert in this type of thing (his company was hired by the government to investigate the collapse of a large hall, under snow I believe), and she shows him the pictures attached to this post. He says this is definitely subsidence! Whether it is ongoing he is unable to say without actually visiting the property. The estate agent friend also said that when she visited properties she always looked at the doorframes and bent doorframes were usually a sign of subsidence.

So what is the dilemma? (Btw, thank you for getting this far!) Well, if this is ongoing subsidence then fine, no use crying over spilt milk, this is what insurance is for. What I am worried about is if this subsidence is old, and not ongoing, i.e. the cause is gone: if the insurance lot come down and make this determination, there won’t be extensive works/costs to them, but they would put a lovely “history of subsidence” on the policy and then changing insurance companies becomes a nightmare and they can charge pretty much whatever they like.

Should I ask the insurance company to commission a structural survey (are my concerns justified?) or should I get a survey done privately (as the estate agent friend suggests) and if there is history of subsidence, but it is not ongoing, perhaps it would be possible just to remove all the evidence (the survey would be a backup to say there is no ongoing subsidence)? Apparently if the survey says it is ongoing (which I think is unlikely) and we then go through insurance, the cost of the survey should be recoverable?

Or is this not subsidence at all? I am totally confused. Thank you for reading! Any suggestions would be greatly appreciated.

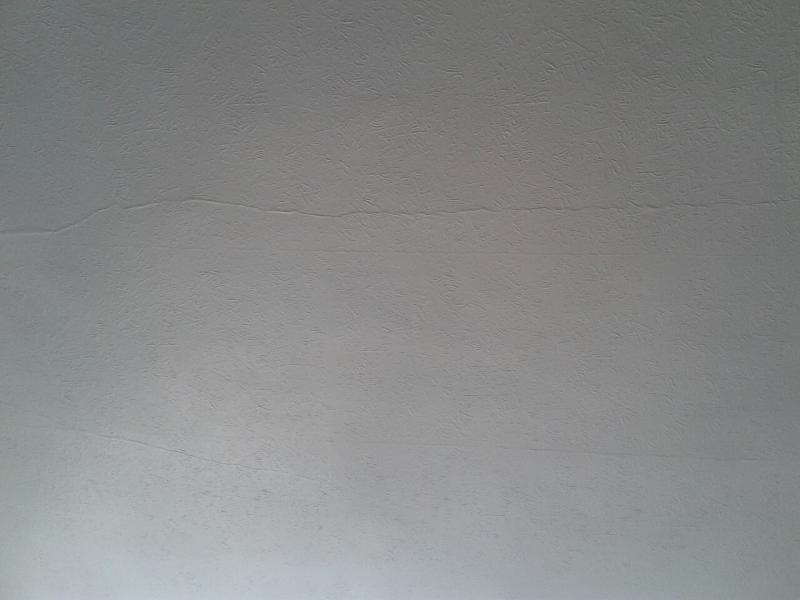

Pictures (pic followed by close-up)

The crack in this picture is 3mm – this is the largest one I believe. Note: the family friend/owner informs me that the door in this picture, which appears crooked, was cut uneven by him, i.e. this here is not a crooked door frame, at least not obviously.

Here you can probably see the crooked door frame.

I am helping an elderly family friend with his home in London. A decorator/builder pointed out cracks and uneven door frames and said this was subsidence. I contacted a friend who has experience renovating houses who (logically I think) advised me to call the insurance company, since we are lay people in this regard and have them take a look to see if it is or it isn't. I did so, but just getting them to evaluate it involved "making a claim" which made me apprehensive.

OK I've descended into a story, so instead I will just summarise what people have told me, which will hopefully be clearer (though you will see why I am very confused). I have included photos of the cracks at the end.

Friend with experience renovating houses: subsidence he associates with cracks from the base of the property, of which there are none (at least not visible) in this case. He says cracks/movements around doors and bay windows are quite common as these are weak points susceptible to settlement.

Neighbour who has been on the road for a long time and pretty much knows about everything that is happening here: he laughed at me saying these are not cracks! He says they have been there for a very long time (this corresponds to what the family friend/owner of the house says) and they are just the result of settlement. He knows only of one house on the street that had subsidence and this was because of a bad tree the council planted (they are – ahem I mean we are – footing the bill) and says he can’t recall there ever being a large tree outside the family friend’s house. He says he has worse cracks that he is not concerned about at all. He warned about getting a ‘history of subsidence’ on a property (this corresponds with what I have read).

Insurance lady: so at this point I call the insurance lady saying how foolish I am and that this is probably nothing. Interestingly she echoed what the friend with experience renovating houses said about no cracks at the base of the property, saying that based on the description I gave this didn’t sound like subsidence to her. She says not to worry, that the insurance claim can be withdrawn and because the value on it would be zero, this should not affect premiums. However, she asks me to get a builder to look at it just to be sure. In hindsight this seems a bit strange since I don’t think the average builder would be qualified to say, or at least would be unwilling to make an assertion, unless perhaps it was very clear-cut, e.g. superficial cracks in the plaster.

Friend (former estate agent) and her friend, an expert in building materials: This is where it gets confusing. So, I contact the friend to ask if she knows a builder that would be suitable. Her friend, in Poland, is an expert in this type of thing (his company was hired by the government to investigate the collapse of a large hall, under snow I believe), and she shows him the pictures attached to this post. He says this is definitely subsidence! Whether it is ongoing he is unable to say without actually visiting the property. The estate agent friend also said that when she visited properties she always looked at the doorframes and bent doorframes were usually a sign of subsidence.

So what is the dilemma? (Btw, thank you for getting this far!) Well, if this is ongoing subsidence then fine, no use crying over spilt milk, this is what insurance is for. What I am worried about is if this subsidence is old, and not ongoing, i.e. the cause is gone: if the insurance lot come down and make this determination, there won’t be extensive works/costs to them, but they would put a lovely “history of subsidence” on the policy and then changing insurance companies becomes a nightmare and they can charge pretty much whatever they like.

Should I ask the insurance company to commission a structural survey (are my concerns justified?) or should I get a survey done privately (as the estate agent friend suggests) and if there is history of subsidence, but it is not ongoing, perhaps it would be possible just to remove all the evidence (the survey would be a backup to say there is no ongoing subsidence)? Apparently if the survey says it is ongoing (which I think is unlikely) and we then go through insurance, the cost of the survey should be recoverable?

Or is this not subsidence at all? I am totally confused. Thank you for reading! Any suggestions would be greatly appreciated.

Pictures (pic followed by close-up)

The crack in this picture is 3mm – this is the largest one I believe. Note: the family friend/owner informs me that the door in this picture, which appears crooked, was cut uneven by him, i.e. this here is not a crooked door frame, at least not obviously.

Here you can probably see the crooked door frame.

") I also forgot to mention it is semi-detached.

I also forgot to mention it is semi-detached.